>>

Industry>>

Fintech and Financial Services>>

Top State-Sponsored 529 Colleg...FINTECH AND FINANCIAL SERVICES

Top State-Sponsored 529 College Savings: Best 529 Plan for Out of State Residents

The Silicon Review

21 January, 2026

Author:

The Silicon Review Team

Choosing a 529 plan can feel like scrolling through endless streaming options while the popcorn cools. Every state runs its own program, yet you’re free to pick any of them—meaning more than 100 choices compete for your tuition dollars.

Many families default to their home state’s plan for a small tax break, but fees matter more. According to a 2025 Savingforcollege study, trimming just 0.25 percentage point from annual expenses can beat a one-time $500 deduction over an 18-year horizon.

So why settle for a middling option when several top-tier plans welcome everyone? We’ll cut through the noise, address common myths, and highlight the state-sponsored 529s that treat out-of-state investors like locals.

New to 529s? Before we get started, skim our partner guide on about 529 plans—it sets the stage for the comparisons ahead.

In the next few minutes, we’ll map today’s 529 landscape, explain our ranking method, and spotlight the standouts—no jargon, no fluff, just clear guidance you can act on now.

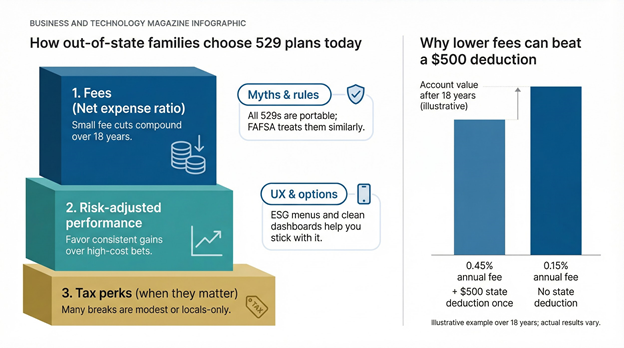

How out-of-state families choose 529 plans today

Cost comes first. Every dollar you pay in expenses is a dollar that never compounds for college. Cutting annual fees from 0.45 percent to 0.15 percent can add thousands to your balance over 18 years, often outpacing a single $500 state deduction, according to a 2025 Savingforcollege analysis.

Performance is next. We favor plans that match or beat broad market indexes without betting on high-cost moonshots. A consistent five-year record backed by a balanced asset mix shows the plan’s stewards can stay on course when markets shift.

Tax perks still play a role, but only when they move the needle. About 17 states offer a deduction for contributions, and nine “tax-parity” states let you claim that break no matter which plan you choose. If you live in California, Texas, or Florida, there is no state income tax to offset, so you can pursue the best plan nationwide with no trade-off.

Myths persist. You are not limited to colleges inside a plan’s state, and FAFSA treats all parent-owned 529s the same. Qualified withdrawals are tax-free everywhere, whether the account began in Illinois, Utah, or Alaska.

Better yet, the industry keeps improving. States trimmed fees again in 2025, expanded ESG and custom-portfolio choices, and rolled out cleaner digital dashboards. With barriers down and quality up, out-of-state investors can shop like pros with zero guilt and zero friction.

What other reviews miss and why it matters

Skim recent “best 529” round-ups and a pattern appears. They mention low fees, toss out a top-five list, then sign off. Useful, yet those lists leave gaps that can cost you real money.

First, most outlets lag on policy shifts. The SECURE 2.0 Act, effective January 1, 2024, lets families roll up to $35,000 of unused 529 money into a Roth IRA after 15 years of account history. Many rankings still overlook this change.

Second, methodology is often a black box. Sites grade plans without disclosing how they weigh fees, returns, or oversight. We show our scoring so you can audit every pick.

Third, governance rarely gets airtime. Consistent state oversight leads to fee cuts and stronger fund menus over time, yet most lists ignore the people steering the program.

Tax nuance also goes missing. Articles tout deductions that apply only to locals, skipping the nine tax-parity states where you can claim a write-off on any plan. For savers in Arizona or Pennsylvania, that rule is worth real dollars.

Finally, investors who value ESG options or modern dashboards get little direction. Programs such as California’s ScholarShare and Utah’s my529 excel here, but generic top-ten posts seldom mention them.

We call out these blind spots because the best decision comes from seeing the entire board, not just the obvious squares.

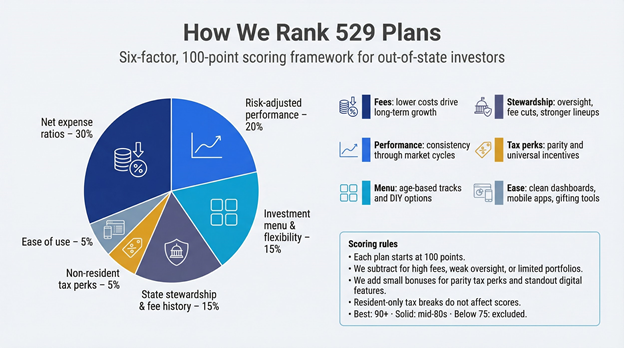

Our 529 plan ranking methodology

You deserve to see exactly how we separate standout plans from the middle of the pack. Transparency keeps us honest and lets you decide whether our priorities match yours.

We pulled fresh data from disclosure documents, independent performance databases, and Morningstar’s 2025 Medalist Report (released October 2025), which names just five Gold-rated 529 plans nationwide. Each program then earned points across six factors that matter whether you live in Maine or Hawaii.

|

Criterion |

Weight |

Why it matters |

|

Net expense ratios |

30 percent |

Lower costs leave more room for tax-free growth. Over 18 years, trimming 0.30 percent a year can add thousands to your balance. |

|

Risk-adjusted performance |

20 percent |

Consistent returns show the plan’s mix and managers can navigate bull and bear markets. |

|

Investment menu and flexibility |

15 percent |

Age-based tracks for hands-off savers plus single-fund options for tinkerers give every family the right fit. |

|

State stewardship and fee history |

15 percent |

Active oversight leads to regular fee cuts and stronger fund lineups, protections many robo rankings overlook. |

|

Non-resident tax perks |

5 percent |

A modest boost if the state offers parity deductions or universal incentives. |

|

Ease of use |

5 percent |

Clean dashboards, mobile apps, and simple gifting tools keep contributions flowing and mistakes low. |

Each plan starts at 100 points. We subtract for high fees, weak oversight, or limited portfolios and add bonus ticks for standout digital features or parity deductions. Scores cluster quickly: the best break 90, solid options land in the mid-80s, and anything under 75 drops off our short list.

Finally, we ignore tax breaks that vanish once you cross a state line. If an incentive helps residents only, it carries no weight here. The result is a ranking focused on value you can tap wherever you live.

Best 529 plans for out-of-state residents

1. Illinois Bright Start 529 College Savings Plan

Bright Start leads for a clear reason: it delivers Gold-level quality at index-fund prices. Its official explainer on everything you need to know about 529 plans points out that earnings grow tax-deferred and qualified withdrawals stay tax-free; those are benefits this plan amplifies with rock-bottom fees.

Morningstar’s 2025 Medalist Report keeps Illinois in its highest tier for the seventh straight year, praising the state’s habit of trimming costs and broadening choices.

Fees sit near rock-bottom. Most age-based index tracks charge about 0.10 to 0.15 percent all-in, so only a dime on every hundred dollars goes to expenses. No enrollment or maintenance fees hide in the fine print.

Choice is equally strong. You can park money in hands-off enrollment portfolios or build a custom mix from eleven fund families, including Vanguard and Dimensional. That range lets tinkerers adjust while set-and-forget savers coast.

Out-of-state investors miss Illinois’s tax deduction, yet the plan’s low costs often outgrow that perk over time. Add responsive web tools and a clean interface, and Bright Start becomes a simple “click, fund, relax” experience with no residency required.

2. Utah my529

Utah’s my529 pairs low costs with deep customization, serving both tinkerers and hands-off savers.

Start with price. Index enrollment tracks charge roughly 0.12 to 0.18 percent a year, savings that compound into real money by freshman orientation. Even portfolios that use Dimensional active funds stay lean.

Flexibility stands out. Build your own mix from Vanguard and Dimensional pieces, adjusting percentages to a single decimal. Want 7 percent international small-cap and 3 percent real estate? Go for it. Prefer one-click “Target Enrollment 2042”? That takes seconds.

Customer experience seals the deal. The dashboard feels modern, contributions land quickly, and the gifting portal turns birthdays into tuition boosts instead of toy clutter. Out-of-state investors lose Utah’s modest tax credit but gain a low-friction engine for growth that works anywhere tuition bills arrive.

3. Massachusetts U.Fund College Investing Plan

If you like set-and-forget with a familiar brand, Massachusetts delivers. The U.Fund, powered by Fidelity index funds, earned Morningstar Gold in 2025, lifting it into the national spotlight.

Costs stay slim. Age-based index portfolios hover a hair above 0.13 percent, placing the plan in the same low-fee league as Illinois and Utah. No program or maintenance charges sneak in later.

The menu remains straightforward. Enrollment portfolios glide from stocks to bonds on autopilot, while a tidy slate of single-fund options lets DIYers fine-tune without analysis paralysis. Fidelity brokerage clients can view their 529 next to IRAs and taxable accounts, turning a yearly check-in into a weekly dashboard glance.

For out-of-state savers, there’s no tax cut and no penalty. You get a lean index engine managed by a household name that keeps trimming expenses. Less drama, more diploma—that’s the Massachusetts angle.

4. Pennsylvania PA 529 Investment Plan

Think of Pennsylvania’s plan as a Vanguard index fund wrapped in college-savings paper. It leans on broad-market funds everyone trusts and keeps total expenses between 0.19 and 0.29 percent, cheap enough that cost never drags on growth.

Recent fee cuts show the state treasury keeps its foot on the gas. Scale helps, too. With billions under management, Pennsylvania negotiates rock-bottom pricing and passes the savings to account holders, resident or not.

The lineup is simple. Age-based Target Enrollment portfolios do the heavy lifting for busy parents. Prefer your own mix? Static options let you dial risk up or down in seconds, all with the familiar Vanguard labels found in many 401(k)s.

Tax perks? Pennsylvanians can deduct contributions to any 529 plan, signalling confidence in open competition. For everyone else, the draw is clear: low fees, index clarity, and a team that keeps shaving expenses.

5. Alaska T. Rowe Price College Savings Plan

Active management often means higher costs, yet Alaska shifts that narrative. By partnering with T. Rowe Price, the plan offers seasoned stock pickers at about 0.50 percent—lean for active funds and backed by long-term outperformance.

The appeal is focus. Age-based portfolios use a tight roster of T. Rowe Price funds that have beaten passive benchmarks more often than not. Savers get growth-oriented equity early on, then a measured glide toward bonds as college nears.

Governance impresses. Alaska’s administrators meet quarterly with managers, scrutinize results, and swap underperformers when needed. That vigilance earned Morningstar Gold, a rare nod for an actively steered lineup.

True, 0.50 percent isn’t the lowest price in this list. But for families who believe skill can add value—and want that edge without managing separate active funds—Alaska offers a ready-made solution open to every ZIP code.

6. Ohio CollegeAdvantage 529 Savings Plan

Versatility is Ohio’s calling card. The plan blends Vanguard index funds, Dimensional factor funds, bank CDs, and a stable-value option, letting you dial risk with surgeon-like precision while keeping most portfolios just under 0.20 percent.

Age-based Ready-Made tracks make life easy for busy parents. Prefer hands-on control? Mix individual funds or place a portion in FDIC-insured CDs for short-term goals. Few plans pair bank-grade safety with market options, a relief for tuition bills due in two years rather than twelve.

Governance stands tall. The Ohio Tuition Trust Authority has run 529s since the 1990s and keeps negotiating fee cuts as assets grow. Recent tweaks lowered admin charges to about 0.12 percent, proof of the state guards every penny.

Ohio residents can deduct contributions to any plan. For everyone else, CollegeAdvantage delivers low fees plus safety and factor-investing tools—a middle ground between pure-index frugality and Alaska-style active flair.

7. New York 529 College Savings Program (Direct)

Sometimes simple wins. New York keeps its entire fee stack to a flat 0.13 percent—no program charges, no maintenance surprises. That thrift alone places it among the national low-cost leaders.

The investment menu is equally clean. Age-based enrollment portfolios glide along a preset path using Vanguard Total Stock, Total International, and broad bond indexes. Prefer a custom mix? Thirteen single-fund options cover every major asset class without clutter.

Scale brings stability. With more than $30 billion under management, New York has the leverage to demand razor-thin costs. The comptroller’s office often secures cheaper share classes, and savers benefit year after year.

There’s no state-level deduction for outsiders, yet no penalty either. You get a simple index ride at a price few rivals match. If you crave minimal effort and maximum efficiency, New York offers a straight path.

8. California ScholarShare 529

California pairs West Coast polish with Midwest-style thrift. ScholarShare’s age-based index portfolios cost around 0.20 percent—slightly above our fee champs but well below the national average.

Usability shines. The web portal feels more fintech than state agency, featuring a clear dashboard, recurring-deposit nudges, and a popular gifting link that lets relatives chip in with ease. Saving becomes as simple as sending a text.

Investment choices strike a balanced mix. Enrollment-date tracks handle glide-path duties, while static options include a social choice (ESG) fund and a principal-protected account for near-term needs. That range serves green investors and safety-first savers without overwhelm.

California offers no contribution deduction even to locals, so out-of-state savers start on equal footing. If you value intuitive design, ESG access, and transparent pricing, ScholarShare belongs on your shortlist.

Side-by-side comparison of our top plans

We’ve covered each plan’s story. Now let’s set the numbers side by side so you can spot differences at a glance.

|

Plan |

Morningstar 2025 rating |

Approx. all-in fee |

Investment highlight |

Extra perk for non-residents |

|

Illinois Bright Start |

Gold |

0.10–0.15 percent |

40-plus portfolio menu, 11 fund families |

Ultra-low minimums ($0 to open) |

|

Utah my529 |

Gold |

0.12–0.18 percent |

Build-your-own custom mix |

Best-in-class gifting portal |

|

Massachusetts U.Fund |

Gold |

about 0.13 percent |

Pure Fidelity index lineup |

Integrated view inside Fidelity.com |

|

Pennsylvania PA 529 IP |

Gold |

0.19–0.29 percent |

Vanguard age-based tracks |

Tax-parity state for future moves |

|

Alaska T. Rowe Price |

Gold |

about 0.50 percent |

Active equity tilt with proven managers |

Tuition credit if child attends UA |

|

Ohio CollegeAdvantage |

Silver |

0.14–0.20 percent |

Vanguard, Dimensional, plus FDIC CDs |

Rare stable-value option |

|

New York Direct |

Silver |

0.13 percent flat |

Simplicity: three Vanguard index funds |

Large asset base helps keep costs low |

|

California ScholarShare |

Silver |

about 0.20 percent |

ESG and principal-protected choices |

Intuitive mobile experience |

Two quick takeaways:

- Fees for every plan on this list sit well below the 0.35 percent national average, so cost won’t eat your returns.

- Morningstar awards only five Gold medals each year; four appear in this table, and all welcome out-of-state investors without strings.

Let the table guide your final pick. If you want the lowest fees, Illinois or New York lead. If customization excites you, Utah wins. Prefer an ESG route? California is ready when you are.

Emerging 529 plans worth a second look

Great programs keep improving, and a few up-and-comers deserve your radar.

New Jersey’s NJBEST lowered expenses in 2025 after switching to Franklin Templeton and added a first-time state deduction. Early performance looks promising, so we’re watching.

West Virginia’s Smart529 Direct replaced several funds with Dimensional options in 2024 and trimmed program fees. Factor tilts plus lower costs could reward patient savers if results stay strong.

Minnesota’s College Savings Plan offers Vanguard and DFA choices at fees near 0.20 percent, yet it remains overlooked by many index fans.

Arkansas’s Brighter Future plan moved to Vanguard target-enrollment portfolios in 2025 and cut costs, earning praise from independent reviewers.

None reach our top eight today, but steady improvement matters. Check back next enrollment season; one of these newcomers could claim a medal.

FAQ: out-of-state 529 questions answered

Do I lose tax benefits if I pick another state’s plan?

No. Federal perks—tax-free growth and tax-free qualified withdrawals—travel with you. The only thing you skip is your home state’s deduction or credit, and in many places that break is modest. Nine tax-parity states (Arkansas, Arizona, Kansas, Minnesota, Missouri, Montana, Pennsylvania, Ohio, and Indiana) let you claim the deduction on any 529 contribution.

Can my child attend college anywhere?

Yes. Savings plans are portable. Money from an Illinois or Utah 529 pays tuition in Maine, Madrid, or an accredited online program, provided the school appears on the federal eligible-institution list.

What if my child never sets foot on campus?

You still have options. Change the beneficiary to a sibling or yourself, apply up to $10,000 toward student loans, or use the SECURE 2.0 rule (effective January 1, 2024) to roll as much as $35,000 into the beneficiary’s Roth IRA after 15 years of account history.

How hard is it to switch plans later?

It is straightforward. One trustee-to-trustee rollover per beneficiary is allowed every 12 months. Open the new account, complete a transfer form, and let the plans handle the wiring. Watch for recapture rules if you claimed a state deduction within the past few years.

Does FAFSA treat out-of-state plans differently?

No. A parent-owned 529 counts as a parental asset regardless of its state label and is assessed at a maximum of 5.64 percent. Distributions are not taxed as income, and recent FAFSA changes make grandparent-owned 529 withdrawals penalty-free as well.

Conclusion

The best 529 plan for your family likely isn’t in your backyard—it’s wherever low costs, strong oversight, and flexible investments intersect. By focusing on expense ratios first and extras second, out-of-state savers can harness tax-free growth without sacrificing returns. Use the rankings and comparisons above as a launchpad, then open the account that aligns with your goals and start funding it today.