>>

Industry>>

Management consulting>>

From Noise to Signal: Building...From Noise to Signal: Building a Fund-Level Operating Model for Systematic Deal Sourcing

The Silicon Review

01 May, 2025

Author:

Dmitry Golomidov, Mento VC, Partner

Far more companies are seeking investors than investors are seeking places to deploy capital. Today there is no scarcity of promising startups looking for capital, and the main issue for investors is how to spot them early enough for the investment to be mutually beneficial. In private markets, information is usually incomplete, slow to surface and often privately negotiated, so the only durable tool is an operating model that turns messy data into a reliable sourcing and selection system.

The “market is always right” mantra works best in public markets that are liquid, relatively transparent and where assets are continuously priced. But venture investors operate before that stage, having to navigate through fragments of truth and patchy data. Research here means designing the way you gather information and structure decisions, not just analyzing what is already in front of you.

Before the Signal

While VC funds have long relied on inbound deal flow and warm introductions, a more systematic and less biased approach means building a structured screening process and applying it consistently at scale. Keeping track of thousands of potentially relevant companies requires an automated system that scans for signals before you decide where to direct attention.

The triggers worth tracking are observable and measurable, and include investor attention maps, search trends, web traffic, follower growth and downloads. They do not replace financials – the core indicators of business health – but serve as pre-filters that narrow the field before any deeper work begins.

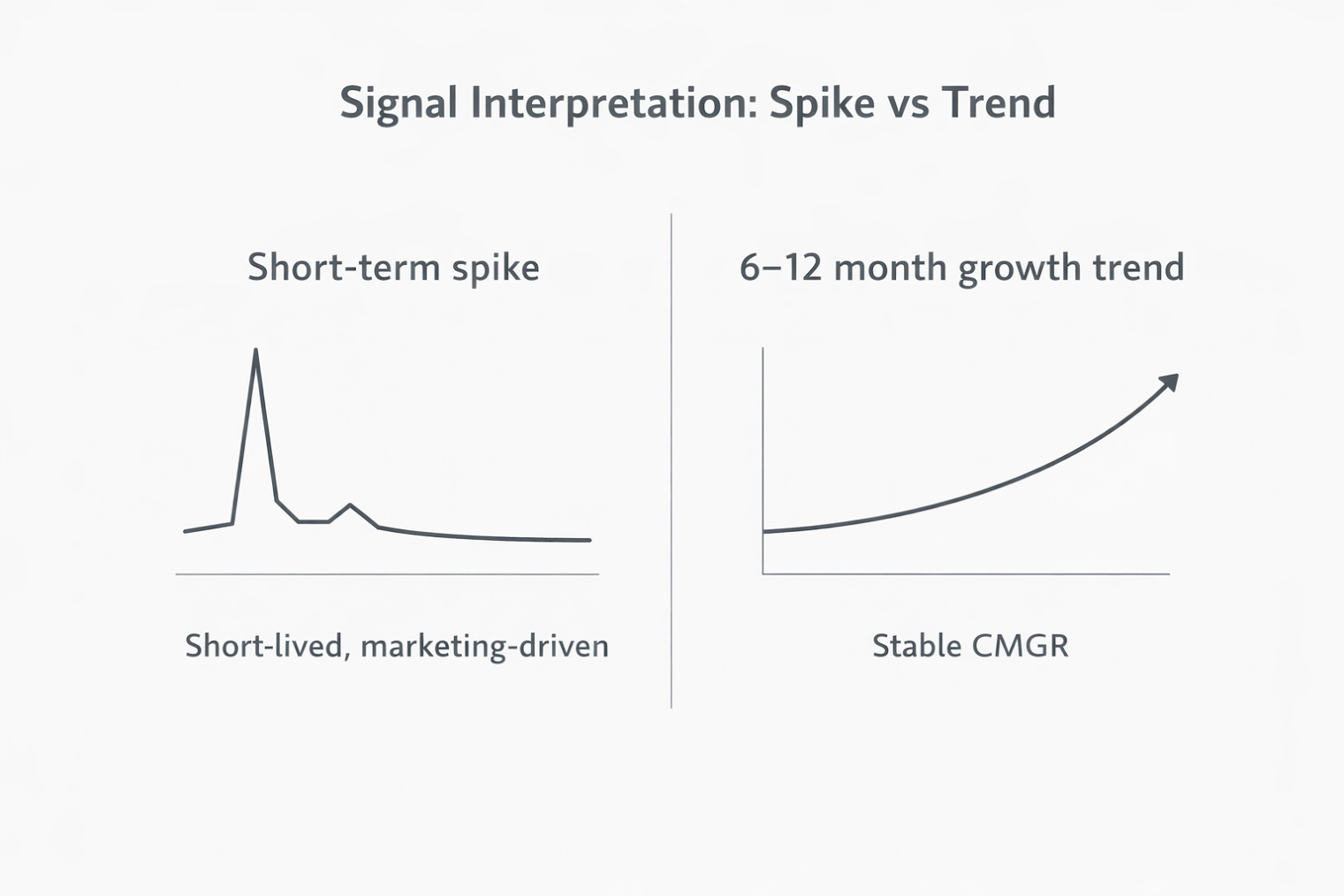

The data behind these signals has to be clean and legally sourced because, when screening at scale, the reliability of the system depends on the quality of its inputs. If the underlying data is reliable enough, it becomes easier to distinguish between a short-lived spike driven by a marketing push and 6–12-month growth trend reflected in a stable CMGR (Compound Monthly Growth Rate).

Tracking the same external proxies month after month makes it easier to see whether growth is holding in, say, the 10-15% range or gradually losing momentum. The same approach also helps identify products with waitlists, early user queues and narrow vertical traction long before they are formally packaged for investors.

Interpreting Flat Metrics

Some companies show flat external metrics not because they are weak, but because the market they are operating in has not entered a real growth phase yet, or has simply not taken off. This is where LLMs can help: grouping companies by segment and customer type makes it easier to distinguish between a business that is going nowhere and one that is simply early.

Context matters just as much at the next stage. In B2B, an investor needs to understand which cost line the product is replacing – a modest software budget or actual headcount. In B2C, the more important question is how often customers pay and whether the product becomes part of a recurring habit. The same growth curve can mean very different things depending on the category the business operates in.

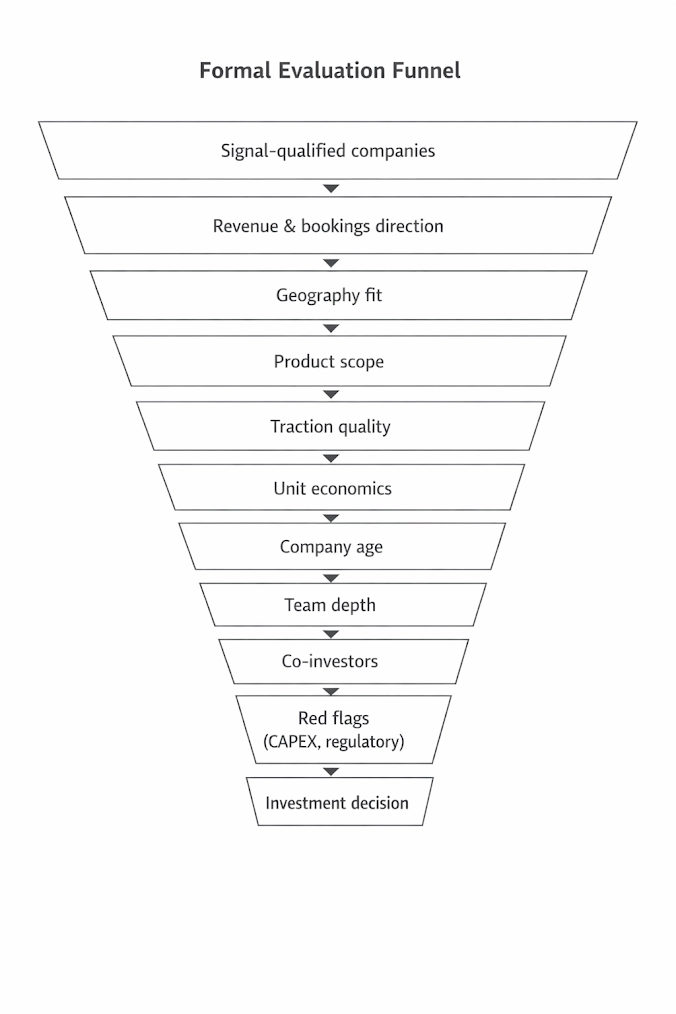

The Formal Funnel

Once a company clears the initial signal thresholds, it enters a more formal evaluation funnel. From that point on, the screening becomes more structured: investors look at revenue and bookings direction, geography fit, product scope, traction quality, unit economics, company age, team depth, the quality of co-investors and any obvious red flags, including heavy CAPEX requirements or regulatory traps.

Applying the same criteria to every company makes the process more disciplined and reduces the inconsistency that often comes with deal-by-deal decisions. Venture has a long feedback loop, so without that kind of structure, it is difficult for a fund to know whether its judgment is improving or simply drifting.

The Founder’s Role

At early stages, the founder is both the main risk factor and the main asset. Investors want to understand how that person approaches growth channels and unit economics, and whether they see a real path to building something exceptional rather than just a slightly faster version of what already exists.

Only then do investors turn to the business itself, where recurring revenue, contract quality, LTV (the total revenue expected from a single customer relationship), retention and margins help them assess whether growth is real or simply expensive.

Thinking About Exit from Day One

Exit should be part of the investment logic from the very beginning, not something left for later once the company has already scaled. That matters because the quality of an investment depends not only on whether a company grows, but also on how and when liquidity can realistically emerge.

Once a company approaches unicorn-type scale, secondary liquidity often becomes available well before an IPO or acquisition, and that possibility should already be reflected in how investors think about the opportunity at entry.

The Funnel in Practice

At Mento VC, these are not abstract principles but part of how a data-driven early-stage investment fund actually operates. The same logic should run through the process from the first signal to the final investment decision, while still allowing for some deviation, because no two investment cases are ever identical.

The point is not to find a compelling story and turn it into a successful deal, but to build a system that helps a fund select consistently across different market conditions. In practice, that means treating models, AI tools and structured sourcing as core parts of the investment process. They do not replace judgment but help investors apply it earlier and more effectively, especially in a market that still relies heavily on warm introductions and more traditional sourcing methods.